Canada's economy in the past year had a bumpy ride, as the promise of mass vaccinations was followed by supply chain disruptions, a global energy crisis and rising inflation.

Looking ahead, we see a Canadian economy continuing to recover, even as businesses and consumers contend with challenges that now include the omicron variant of the coronavirus. Here's what we forecast for the economy

this year:

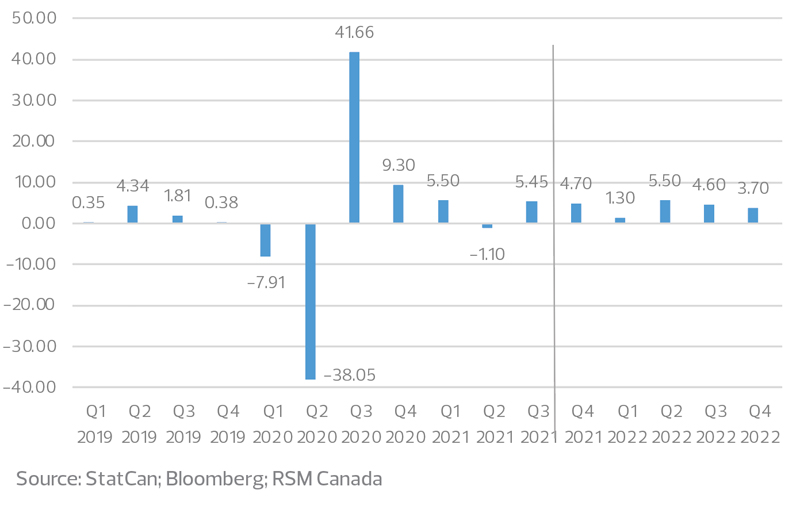

- Gross domestic product: Growth will be just under 4 per cent on the year, with gross domestic product surpassing the pre-pandemic level early in the year.

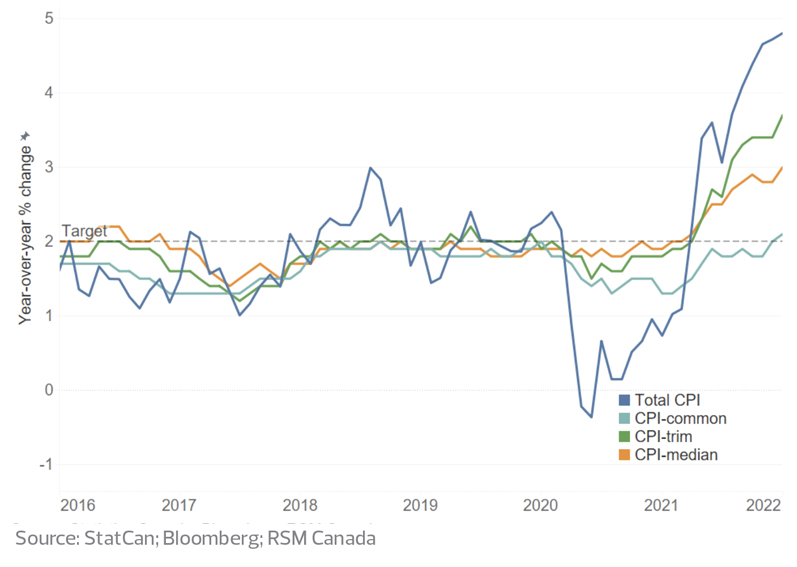

- Inflation: Expect inflation to hit 5 per cent this year before approaching 3 per cent by the year's end.

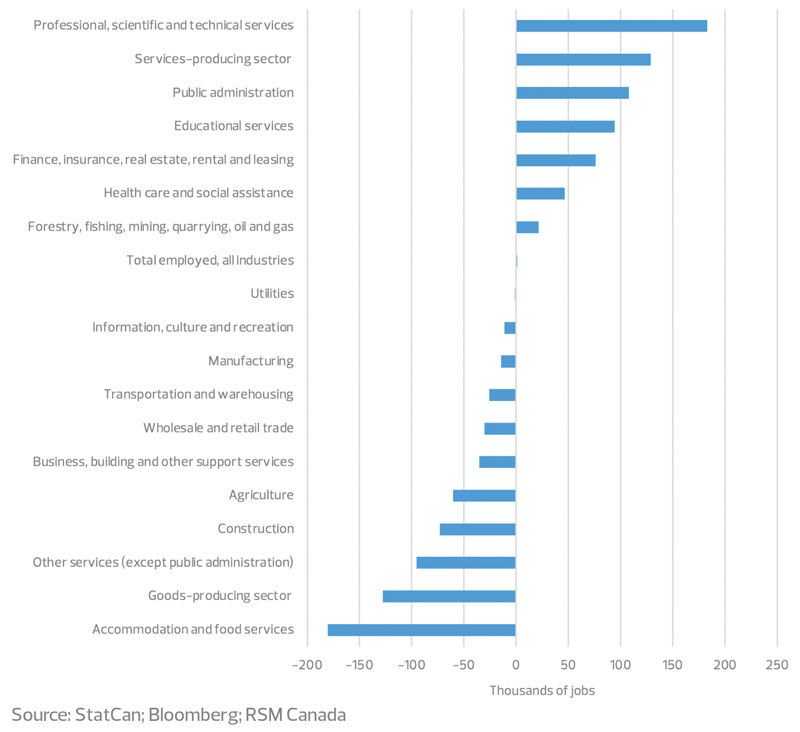

- Employment: The job market will continue to contend with the dual challenges of a tight labour market and high long-term unemployment, as the unemployment rate declines to just above 6 per cent.

While the omicron variant presents a threat to all these areas of the economic outlook, we do not expect its impact to significantly derail the recovery.

The housing market, which broke records this past year, might hit a plateau and cool this year, but a major correction is not yet in the picture.

After an uneventful election in September that left the federal government virtually unchanged, we can expect federal spending to follow its budget from last April.

Broad-based COVID-19 government support programs ended this year, and more targeted support programs will also be phased out in place of economic stimulus programs before the budget is tightened next year.

The year ahead will also have substantial federal investment in developing a net-zero economy and boosting a green recovery. Business opportunities lie in energy efficiency, carbon capture and storage technology, natural infrastructure, and climate resiliency.

Still, there are considerable risks to the outlook some that cannot be predicted. The omicron variant is a case

in point.

Canada will need to adapt to a new world in which we learn to live with an endemic, a disease that is ever-present but can be managed. It's a world in which vaccinations and physical distancing remain important to maintaining public health while the economy hums on.

As millennials enter management and Gen Z workers join the labour market, the digital economy will only continue to grow. Hybrid work arrangements and flexible schedules will solidify their footing in the new normal. Upskilling and reskilling the workforce and innovation to increase productivity will be critical.

The baseline scenario

We expect the Canadian economy to grow at a rate of 3.8 per cent next year. This baseline is subject to risks including persistent high inflation, supply chain disruptions, the omicron variant and an aging workforce. Any and all of these could cause a drag on the recovery.

Household savings increased during the pandemic, fueled by government support programs like the Canada Emergency Response Benefit and a lack of spending avenues that put the savings rate at an elevated 11 per cent.

This cash cushion will allow households to comfortably spend into this year, although the effects will wane with high inflation and the omicron variant posing a risk to consumer confidence.